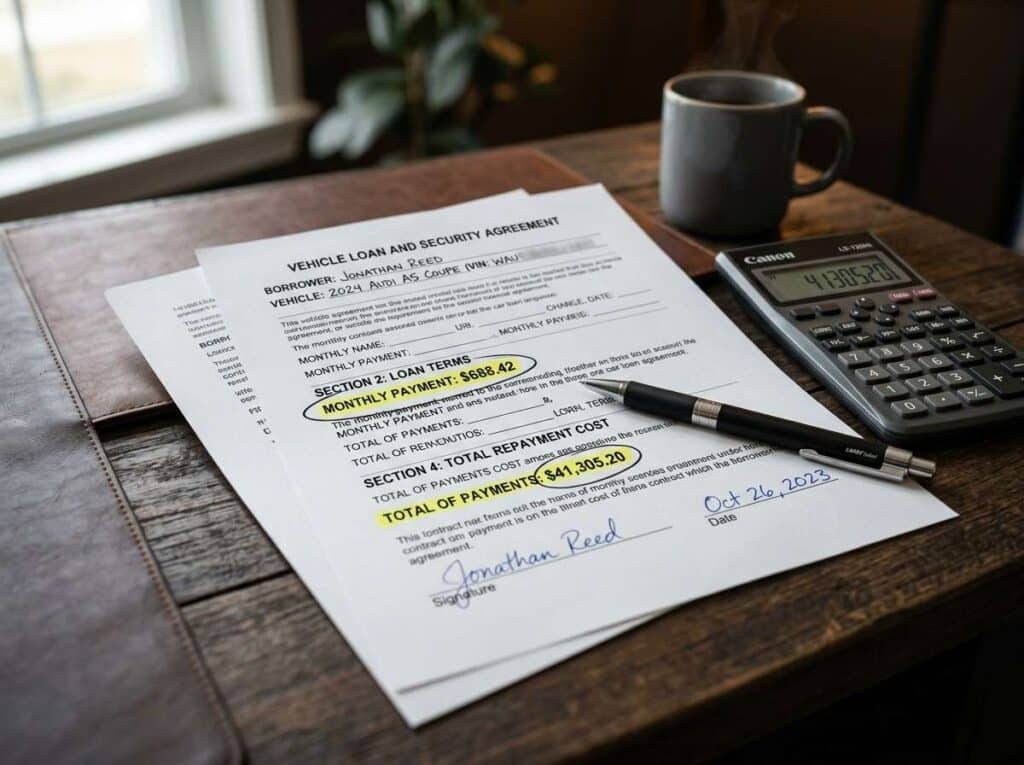

You’re sitting in the finance office. The salesperson just handed you off, and suddenly the numbers look different. The monthly payment still works. But the total cost quietly jumped by $3,200. This specific figure represents the average “stealth markup” found in complex financing contracts where back-end products are bundled without clear disclosure, according to the Consumer Financial Protection Bureau 2026 Auto Loan Report.

This is where most people lose track of the deal. Over eight years working inside dealerships, I watched the same three moments trip up buyers again and again. Not because they weren’t smart — because the process is built to shift your focus at exactly the wrong time.

By the end of this, you’ll know where the real money slips away, how much it typically costs you, and what numbers to watch instead. We’re grounding this in data from the Federal Reserve 2026 Consumer Credit Report, Kelley Blue Book, and Edmunds’ True Cost to Own estimates. And yes — some deals are fair. But these three moments are where they stop being fair.

1. The Monthly Payment Trap — Where $0 Down Can Cost You $4,000+

The salesperson asks one simple question: “What monthly payment are you comfortable with?” It seems harmless. It isn’t. According to the Consumer Financial Protection Bureau, focusing on monthly payment instead of total loan cost is one of the most common ways buyers overpay — often by extending loan terms or increasing interest without realizing it.

Here’s what that actually means for your wallet.

| Loan Scenario | Monthly Payment | Loan Term | Total Interest Paid |

| $30,000 loan @ 5% | $566 | 60 months | $3,968 |

| Same loan stretched to 72 months | $483 | 72 months | $4,776 |

| Same loan at 8% (credit impact) | $608 | 60 months | $6,496 |

That lower payment looks good. The five-year cost doesn’t. And this is where buyers drift. The conversation shifts from price to comfort. Dealers know most people anchor on monthly affordability, not total outlay. I’ve seen buyers approve a deal that added $70 a month of hidden cost — because the payment stayed within their “range.” This $70 jump, when applied to a 72-month term, adds over $5,000 in total cost due to compounding interest.

The better question to ask: what is the total amount I am paying over the life of this loan? Sit with that one.

2. The Trade-In Undervaluation — Losing $1,500 Without Noticing

You probably walk in thinking your trade-in will “help lower the price.” That’s true. But it’s also where quiet losses stack up. According to Kelley Blue Book, trade-in values can vary by thousands depending on timing, condition, and negotiation. And most buyers don’t separate the trade from the purchase — which is exactly how dealers bundle the math.

| Vehicle | KBB Trade-In Range | Dealer Offer | Difference |

| 2018 Honda CR-V EX | $17,500–$19,000 | $16,000 | $1,500 to -$3,000 |

| 2017 Toyota Camry SE | $13,200–$14,500 | $12,000 | $1,200 to -$2,500 |

| 2019 Ford Escape SEL | $16,000–$17,800 | $14,500 | $1,500 to -$3,300 |

That gap often gets buried inside the deal. Dealers may increase your trade value slightly — then raise the price of the new car to offset it. Net result? You still lose money, but it feels like you “won” the trade negotiation.

In my experience, buyers who negotiated their trade-in separately — or got outside quotes from places like CarMax or KBB Instant Cash Offer — consistently came out ahead. If you don’t know your trade’s real market value walking in, you’re negotiating blind.

3. The Finance Office Add-Ons — Where $2,000 Turns Into $5,000

You’re almost done. Papers are printing. Then comes the final conversation. Extended warranties. GAP insurance. Paint protection. Tire packages. Some of these can be useful. Most are overpriced.

According to the Federal Reserve 2026 Consumer Credit Report, the average auto loan balance has steadily increased, partly due to add-ons rolled into financing — which means you’re paying interest on them, too.

| Add-On Product | Typical Dealer Price | Estimated Fair Market Cost |

| Extended warranty | $2,500–$4,000 | $1,500–$2,200 |

| GAP insurance | $800–$1,200 | $300–$600 |

| Paint protection | $700–$1,200 | $200–$500 |

| Tire/wheel protection | $900–$1,500 | $400–$800 |

Stack two or three of these, and you’ve added $3,000+ to the loan. Now add interest over 60–72 months. That $3,000 can quietly become $4,000–$5,000 in real cost. GAP insurance can make sense if you’re putting little money down and financing long-term, but the dealer price usually isn’t the best price.

In our assessment, extended warranties are the most commonly oversold product — especially on brands with strong reliability data from Consumer Reports. Many buyers never use them. Still, your mileage may vary. If you’re buying a vehicle with a weaker reliability history or plan to keep it long past warranty, the math shifts.

The Compounding Effect — Small Decisions, Big Money

Individually, these moments don’t look catastrophic. Together, they stack. Here’s a simplified example of how one deal can drift:

| Cost Area | “Good Deal” Scenario | “Typical Drift” Scenario |

| Loan structure | $3,968 interest | $6,496 interest |

| Trade-in value | Full KBB estimate | -$2,000 loss |

| Add-ons | $0–$800 selective | $3,500 bundled |

| Total difference | — | +$5,000 to $7,000 |

That’s the gap. Not from one bad decision. From three small ones. And the tricky part? Each one feels reasonable in isolation.

So Where Should You Push Back?

If you only fix one thing, fix the loan structure. That’s where the biggest long-term cost sits, and it’s the easiest to lose control of. Use tools like the Edmunds’ True Cost to Own calculator before you walk in — it forces you to think in total dollars, not monthly comfort.

Next, separate the deal into three parts:

- Vehicle price

- Trade-in value

- Financing

Dealers prefer blending them. You want clarity. And finally, pause in the finance office. You’re allowed to say no. You’re allowed to take time. That pressure to “wrap it up” is where the most expensive decisions happen.

Conclusion: The Buyers Who Spend Less Do One Thing Differently

Buyers who come out ahead don’t negotiate harder. They stay focused on total cost. If you’re choosing where to concentrate your effort, prioritize the loan first, then the trade-in, and treat add-ons with skepticism unless you’ve priced them independently. Based on the data here, that order consistently saves the most money.

I’ll be honest about one limitation: this article can’t account for regional pricing swings or inventory shortages, which can change how much leverage you have. In tight markets, even well-prepared buyers may pay more. However, the structure of the deal does not change.

Before you step into a dealership, run your numbers through Edmunds TCO, check your trade value on KBB, and review financing basics through the CFPB. These steps help provide the necessary transparency to keep thousands of dollars in your pocket — without changing the car you buy.

References

- Consumer Financial Protection Bureau 2026 Auto Loan Data

- Federal Reserve 2026 Consumer Credit Report

- Edmunds 2026 True Cost to Own (TCO)

- Kelley Blue Book 2026 Trade-in Values

- Consumer Reports 2026 Car Reliability Guide

Disclaimer

Disclaimer: The information provided in this article is for educational and informational purposes only. It does not constitute professional advice. Readers should conduct their own research and consult with qualified professionals before making any decisions.