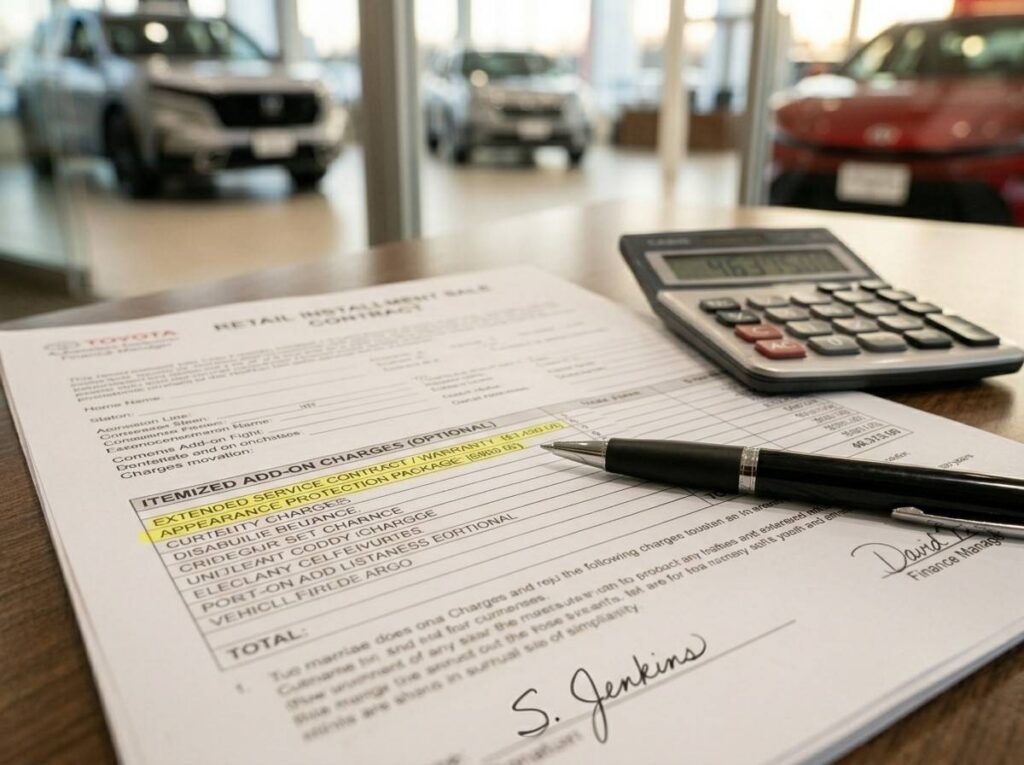

You’ve agreed on the price. Then the finance office adds $2,400 back in.

It happens fast. The monthly payment barely moves — maybe $38 more — and suddenly you’ve bought three products you didn’t plan on. According to the CFPB’s 2026 auto lending guidance, add-ons are one of the most common ways buyers end up paying more than expected over the life of a loan.

Here’s what that actually means for your wallet: that extra $2,400 often turns into $3,000+ once interest is applied over a five-year loan. This guide walks through the most common dealership add-ons, what they typically cost in the U.S., and when — if ever — they make financial sense. We’ll lean on data from Edmunds 2026 True Cost to Own, Kelley Blue Book 2026 pricing insights, and Federal Reserve 2026 credit trends to keep it grounded.

And more importantly, how to say no without blowing up the deal.

Extended Warranties: $1,200–$3,500 for Coverage You May Never Use

The pitch sounds reasonable. Modern cars are expensive to fix.

But most new vehicles already come with a 3-year/36,000-mile bumper-to-bumper warranty and a 5-year/60,000-mile powertrain warranty. Brands like Hyundai and Kia go even longer. You’re often paying for overlapping coverage in the early years.

Here’s the math for common 2026 models.

| Vehicle Example | Factory Warranty | Typical Extended Warranty Cost | Likely Overlap Period |

| 2026 Toyota Camry | 3yr/36k basic | $1,800 | First 3 years |

| 2026 Honda CR-V | 3yr/36k basic | $1,500 | First 3 years |

| 2026 Ford Escape | 3yr/36k basic | $2,200 | First 3 years |

According to Edmunds 2026 True Cost to Own estimates, average maintenance and repair costs in the first five years for these vehicles often stay under $2,000 total. This means many buyers never recoup the warranty cost.

In our assessment, extended warranties make sense only if you plan to keep the car well past factory coverage — think 8–10 years — and the price is aggressively negotiated down. Otherwise, it’s insurance you may never use.

Short version: decline it at signing. Revisit later if needed.

Paint Protection and Fabric Coating: $800–$1,500 for a $20 Job

This one shows up under different names — “environmental protection,” “interior guard,” or “ceramic shield.”

The margin is huge.

Dealers often charge $1,000+ for coatings that cost them a fraction of that. While professional ceramic coatings can be worth it in some cases, the dealership version is usually a basic application done quickly.

Kelley Blue Book 2026 pricing guidance suggests similar aftermarket treatments can be purchased independently for far less, often under $200 if you DIY or $300–$500 professionally.

Here’s the reality: you’re paying a 200%–400% markup for convenience.

I’ve watched buyers accept this because it’s framed as “protecting your investment.” Fair idea. Bad pricing.

If you care about paint protection, do it after purchase — on your terms, not theirs.

GAP Insurance: $500–$1,200 vs. $10/Month Elsewhere

GAP (Guaranteed Asset Protection) covers the difference between what you owe and what the car is worth if it’s totaled. It’s one of the few add-ons that can make sense.

But the dealership version is often overpriced.

The Federal Reserve’s 2026 consumer credit data shows longer loan terms — 72 months and beyond — are increasingly common. That increases the risk of being “upside down” on a loan, which is exactly what GAP protects against.

Here’s the catch: your auto insurer usually offers the same coverage for about $5–$15 per month.

| Source | Typical Cost | Total Over 5 Years |

| Dealership GAP | $800 upfront | $800 + interest |

| Insurance company GAP | $10/month | ~$600 |

Same coverage. Lower cost.

In our assessment, GAP is worth having if you’re putting less than 20% down or financing longer than 60 months. Just don’t buy it in the finance office.

Wheel and Tire Protection: $600–$1,200 for a Low-Probability Event

You’ll hear this framed around potholes. Especially in cities with rough roads.

Fair concern.

But most plans come with strict exclusions — cosmetic damage, wear and tear, and certain road conditions may not be covered. Claims often require documentation that turns small issues into a hassle.

According to Edmunds 2026 ownership estimates, average tire replacement over five years for mainstream vehicles typically runs $600–$1,000 total. That is for normal wear, not damage.

So you’re prepaying for something that may never happen, at a price similar to just handling it out of pocket.

If you’re driving low-profile tires on a performance car, maybe reconsider. Otherwise, skip it.

VIN Etching and Theft Protection: $200–$400 for Minimal Impact

This one feels official. It’s not.

VIN etching — engraving your vehicle identification number onto the windows — is often presented as a theft deterrent. Some dealers bundle it into “security packages.”

Law enforcement agencies do acknowledge that etching can help with recovery. But many police departments offer it for free or low cost.

And insurers rarely give meaningful discounts for it anymore.

So what are you actually buying?

A small layer of deterrence. At a markup.

This is an easy no.

The Payment Trap: Why Add-Ons Slip Through

The monthly payment looks fine. The five-year cost doesn’t.

Dealers often present add-ons in terms of monthly impact — “this only adds $27/month.” It sounds small because it is, in isolation.

But stack three or four of these, and you’ve added $100+ monthly. Over 60 months, that’s $6,000.

Here’s the question buyers rarely ask in that moment:

What’s the total cost of this add-on over the life of the loan?

Sit with that.

Because once you frame it that way, most of these products fall apart quickly.

Add-On Reality Check: What’s Worth It vs. What Isn’t

Not all add-ons are bad. Some are just overpriced versions of useful products.

Here’s a quick breakdown grounded in typical U.S. pricing:

| Add-On | Typical Dealer Price | Real-World Value | Recommendation |

| Extended Warranty | $1,200–$3,500 | Low early, higher long-term | Usually decline |

| Paint/Fabric Protection | $800–$1,500 | Low | Decline |

| GAP Insurance | $500–$1,200 | Moderate | Buy elsewhere |

| Tire/Wheel Protection | $600–$1,200 | Low for most drivers | Decline |

| VIN Etching | $200–$400 | Minimal | Decline |

This is where buyers lose money. Quietly.

And to be fair, there are edge cases. If you’re financing with minimal down payment in a high-depreciation vehicle, GAP becomes more relevant. If you plan to keep a car past 100,000 miles, extended coverage can have value.

But those are exceptions, not defaults.

How to Say No Without Killing the Deal

You don’t need a speech. You need a script.

“I’m declining all add-ons today.”

That’s it.

If pushed, repeat it. Calmly. The finance manager may try to reframe or bundle — separating each product into small monthly increments again.

Stay anchored to total cost.

In my experience on the dealership side, buyers who are polite but firm move through the process faster and with fewer extras. The system expects resistance. It doesn’t expect clarity.

Where the Real Cost Shows Up Later

According to Edmunds 2026 True Cost to Own, depreciation alone accounts for roughly 40%–50% of a vehicle’s five-year cost. Add-ons don’t increase resale value in most cases.

So that $2,000 in extras?

It’s almost entirely sunk cost.

And if you financed it, you’re also paying interest on something that adds zero resale value. The CFPB’s 2026 auto lending guidance has flagged this dynamic as a common source of negative equity in auto loans.

This is a big deal.

Because it affects your next trade-in, your loan balance, and how much flexibility you have when you want to switch vehicles later.

What to Decline — and What to Reconsider Later

If you want the clean version: decline everything in the finance office, then reassess separately.

Buyers who do this tend to spend thousands less over the life of a loan. Not because they avoided every product forever, but because they bought only what they actually needed — at market prices, not dealership markups.

In our assessment, the only add-on worth serious consideration is GAP insurance — and even then, only under specific financing conditions. Everything else can wait.

There’s one limitation here. Pricing and coverage terms vary by dealership, region, and lender, and some manufacturers bundle protections differently, which can change the math slightly. So it’s worth checking the fine print before making a final call.

Next step is simple: before you walk into a dealership, run your numbers using Edmunds’ 2026 True Cost to Own calculator and check fair pricing on Kelley Blue Book 2026. Walk in knowing your total budget — not just your monthly payment — and those add-ons lose most of their power.

References

- CFPB 2026 Auto Loans

- Federal Reserve 2026 Consumer Credit

- Edmunds 2026 True Cost to Own

- Kelley Blue Book (KBB) 2026

- EPA 2026 Fuel Economy Data

Disclaimer: The information provided in this article is for educational and informational purposes only. It does not constitute professional advice. Readers should conduct their own research and consult with qualified professionals before making any decisions.